If you’re a product of the ‘70s as I am, you know that there was no shortage of superlative advancements that occurred in that decade. We had just come through one of the most tumultuous civil rights and religious movements in the history of the country, and folks were ready to double down on America. Music, Arts, Science, Food production, Education…and my personal favorite: Star Wars…

Together, they all created the framework upon which our current society was built. But we didn’t always pierce the target when aiming for greatness. In a few cases, our “advances” impaled themselves on the wall instead of hitting the dartboard.

In this post, I’m going to explain why two of these “misses” have been defrauding the Public Trust since the 70’s, and why trusting the media “wisdom” about them may ruin your retirement plans. To what items do I refer? Your IRA and 401(k).

Plus, find out how we can coach you to grow your net worth for FREE.

The Origin of the IRA and 401(k)

Both of these so-called “retirement plans” found their origins in the 70s. IRAs found their genesis in the ERISA Act of 1974. The new 401(k) section of the Internal Revenue Code was written in from the Revenue Act of 1978. According to myth, these changes aimed to deal with the rampant “executive benefits” which permeated corporate America – and helped with the 1976/1980 elections.

But the reality of it is far more insidious.

When the GIs from World War II came home, they, generally, did not have a great deal of stored wealth. Having to leave their jobs, businesses and factories to fight overseas, these men returned to the forced rebuilding of not only their own lives but the nation in general. As a result, these extremely practical, war hardened men, had no interest in gambling their assets in a market for which they had little knowledge and little belief of its benefits. Especially with high-speed trading and internet connections being the stuff of science fiction, putting money into markets for self-maintenance was not thought to be a good idea.

The Deception

Since the intent of the markets is to take (steal) retail traders’ money, and since the market makers were having liquidity issues after the war due to little capital influx, they developed a scheme to have the working class be “forced'' to give over their assets to the markets – without the ability to withdraw their money without severe penalties. This would dump ongoing billions of dollars into the markets for makers to make money, as always, on the backs of hard-working Americans.

These schemes took years to pass through Congress, but once done, they fell into the forms for which we are so familiar: the IRAs and 401(k). These two Trojan Horses have been touted since as the solution to the American dream of retirement. And while they found their inception in a time where it was reasonable to assume a man might work for 40 years for a single company and retire at 62, even then it was simply and quietly supporting a system whose job it was to reduce the wealth of Americans for their own gains.

To be fair, there is a benefit for supporting the system as an employee by giving your money to these two schemes in the form of a credit called a “Saver’s Credit.” This credit is allowed up to 50% of the first $2,000 “donated” into this system for qualifying taxpayers (I say donated because we’re just gifting money into the system for so doing). This means you get $1,000 maximum credit for donating $2,000 or more.

Whooppee.

Lose, Lose

This credit arrives in the form of a reduction of your tax. If you have more credit than you have tax, you do not get a refund of the difference; it would just bring your tax to zero. This is the same whether you donate to an IRA or a 401(k) or if you donate to all of them at once; it’s still $1,000 max.

The purpose of all of the schemes below is to deploy tax-payer labor into the market where, hopefully, such investments will render a return in parallel or better with the growth of the market. However, there is no protection or insurance to return lost capital from poor investment, capital loss, or otherwise. And profits from traditional IRAs and 401(k)s are taxed as ordinary income. So, if you lose, you lose. If you win, you lose. Nice.

The Saver’s Credit

Another insidious deception is the concept of the “tax credit” for donations outside of the measly “Saver’s Credit.” Both traditional IRAs and 401(k)s allow for up to 50% of the allowable amount donated to these accounts to receive a reduction to the taxpayer's AGI.

What’s not typically talked about is the 50% is reduced to 20% when your AGI rises above $43,500 (2023). It continues to dwindle until you receive ZERO credit if your AGI is over $73,000.

This fundamentally renders useless the credits offered low to upper middle-class Americans whose AGIs are in this range and above. Without this credit, all that happens in these traditional programs upon donation, is the taxpayer is locking up their money with dire consequences for its early withdrawal in order to enjoy the same market risk and possible capital gains as if they had just put their monies into buying the S&P itself.

Except that, had they just bought stock, they would have received additional dividends and enjoyed full control of their assets. It is a lose/lose about which very few employers speak to their employees. I'll explain each account class in more detail below.

IRAs

IRAs are not mandatory for employees, and the creation of an IRA requires the use of a broker or firm. But the media and “conventional wisdom” touts their validity and importance to the destruction of many.

The traditional IRA is a scheme where taxpayers get a credit for “donating” money from their labor into a “professionally managed” market-based account. This credit subtracts an equal portion of the taxpayer's Adjusted Gross Income. This scheme is really only a tax deferral on the monies earned in this “account.” Once those monies are distributed (after a certain age), they are taxed as ordinary income.

The only benefit to having your money in this scheme is the donation credit. Monies held in the IRA cannot begin to have distributions to the holder until they reach 59 ½ years old. There are also donation maximums that cannot be exceeded, else additional donations will not receive the tax credit.

Worse, any premature distribution or withdrawal are met with the steepest taxes up to 50% of the value of the principal in addition to taxes levied against profits. They don’t want you taking their money out of that account before you’re too feeble to use it. Except for deployment of funds within the approved IRA account, there is no way to use the funds as collateral against any external deployment of value (like a loan).

There is NO REAL ADVANTAGE to having one’s money locked up in a traditional IRA given the current inflation. See the calculations below.

401(k)

401(k) donation is compulsory for most employees and requires a portion of their labor to be appropriated by the employer’s chosen fund and spent into the coffers of the elite for trade. Although 401(k) plans typically have less investment options as contrasted with IRAs, they have far more flexibility for deployment as collateral.

In fact, the holder of a 401(k) can use the accumulated value of their account as collateral to generate a loan for up to 50% of its value capped at $50,000. This can be extremely advantageous to the resourceful employee as seen below.

For example: that employee could withdraw $50,000 from a bank on a loan which might cost 8% in interest but place it into a crypto investment which makes them 25%/yr for a total of 17%. If this was 50% of the account, now the account is making 13% instead of 8%. 401(k) donation annual maximums are several times higher than IRAs. 401(k)s suffer the same laughable credit allotments and “deferred tax” on their profits as traditional IRAs.

ROTH

The Roth designation is attached to both IRAs and 401(k)s. It is a scheme which is substantially similar in scope and purpose to the traditional iteration with a few exceptions: donations to the Roth account are on after-tax dollars and no credit is given (although the Saver’s Credit is still available).

However, once distributions begin, all profits earned in the Roth are received tax-free. Also, several situations allow Roths to be self-directed which means Roth assets can be deployed by the account holder for real estate, stock and options investment far more flexibly than the traditional choices. An iteration of these “retirement” programs is the somewhat rare “Roth 401(k),” which allows the combination of donation credits, Saver Credits and tax-free distributions of profit for a “best of all worlds” scenario – in what is essentially a bad scenario as described below.

One of the otherwise hushed-about tricks for traditional IRA holders is to “roll over” traditional IRAs (where there was a donation tax credit) into Roth IRAs where profits are distributed tax-free. This method allows for at least a true tax-exempt possibility instead of hybridized tax deferments. This, generally, achieves the same result as a Roth 401(k).

All forms of accounts have their advertised value predicated on the promise of “tax-free” retirement income (not true - except for Roth 401(k)) and the ability to “generate income from the markets” which is also generally not true considering inflation.

Some Cold Hard Math

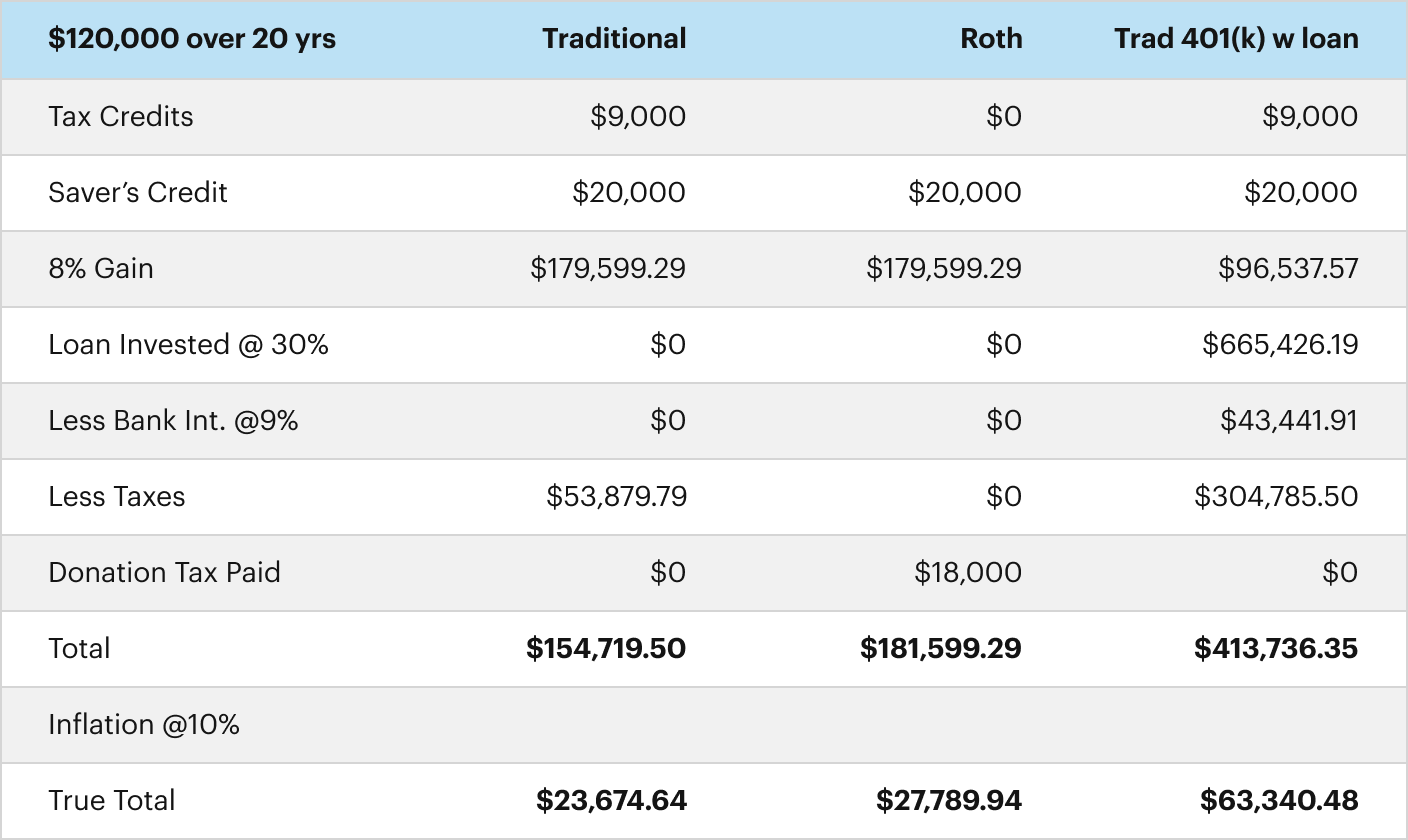

To fully understand the deception here, let’s do a little math. Consider someone who, over 20 years, donated $6,000/yr into their “retirement funds” and had an AGI under $43,000. This would be a total of $120,000 in principle into each account. Let’s see how they stack up against each other in the end. We’ll imagine this person has achieved sufficient age to begin taking distributions without penalty, and they withdraw it all (which is very possible) and assume a 15% tax bracket.

This would mean they would receive $1,000/yr in Saver’s Credit off their taxes + a $3,000/year donation credit on traditional accounts which translates into $450/year @ 15% tax bracket for donation tax and the usual tiered tax for profits up to 40%. We’ll also factor in the market doing 8% a year. Lastly, we’ll factor in a loan started 10 years into the 20 year example on 50% of the principle and earned amounts in a traditional 401(k) where the investment is put into real estate making 30%/yr. with 9% interest from the bank:

It’s pretty exciting to see all those hard-earned dollars multiplying in retirement. The obvious winner in these examples is an external investment of the 401(k) via loan; by far and away. And although a 30% investment per year would beat just about any market strategy as well, that return is not that outlandish given…

Inflation

If the entire purpose of all of these strategies is to beat inflation, taxes and store up value, given our inflation issues, no amount of tax sheltering is going to solve the financial destruction of what locking one’s capital into a government “promised” program at “market rates” will wry on one’s retirement.

I would submit that they’re lying about the inflation rate at 13%. It is FAR HIGHER by the sheer rise in the price of bread in the last 12 months. In my neck of the woods in Tennessee, it’s doubled. So, conservatively, a 10% rate should give us a pretty good sense of what’s real in the economy. And as to how long this rate might go on given our 20 year event horizon? In the 80s, inflation was deep into the double digits for years.

I consider a 10% average over the next 20 years a reasonable barometer of the financial weather. That said, the same $6,000 invested per month after the tiered federal tax rate in a non-income-tax state renders $1,239,445.24 in total assets held. With a 10% inflation rate over those 20 years?

$189,711.44 in value is what you have left after 20 years of investing your $6,000/month @ 30%.

We’re only $70k more than the capital required to invest it. And, quite frankly, that’s a pretty darned good return. FAR SUPERIOR to anything in the IRA/401(k) columns. Remember, this takes into account FULL TAXATION without any tax benefits. And here, you have full control of your money, you’re paying the required taxes, and the money is coming to you at any point you wish – without penalties. Moreover, you can loan out yourself this capital to increase your earnings if you wish.

The Hard Facts

Given our inflationary state of affairs, tax deferred or exempt plans in the marketplace are not worth the weight of paper they require to sign them. Finding a direct source to invest capital, in my opinion, is the only course toward preserving value.

I hope you’re realizing my point here, even if you doubt the inflation rate staying as high as I’ve surmised, or if you doubt my tax calculations on the simulated earnings listed above: government supported retirement programs are a TRAP. Even if I’m 40% wrong, they’re still a trap.

I’ll leave you with this last tidbit: in my Enrolled Agent training, one of the things they stressed is that, although the IRS may say things like “we will never change this again,” “We’ve permanently established this…” even with respect to Americans’ retirement plans they always caveat those statements with this cunning phrase, “until we need to change it.”

Don’t expect the agreement you executed with the government and the IRS (because that’s with whom your agreement is made) to stay the same; not when they can change it willy-nilly. And, besides, what would you do if they did? What could you do?

Can We Help YOU?

Here at Capitalism.com, we are a wealth education company. We teach people how to find their own freedom so they can be their best selves.

In fact, we’re on a mission to make one million new millionaires by 2028. We’d love YOU to be on that list.

That’s why we made this FREE course that will help you grow your own net worth, starting wherever you are right now. Join us and let’s get started.

About the Author

Mark Edward Lewis is a facilitator for crypto tax issues and lectures regularly on the subject of preemptive actions corporations and individuals can take to reduce income and capital gain taxes. He lectures weekly on the subject of crypto taxation, incorporation and how to create funding from banks in his “The Finance Rebellion” series. He is an influencer in several fields including media production, personal development and market analysis." You can follow him on TikTok, Twitter, Instagram, YouTube, and Facebook.

Disclaimer: The views, opinions, and strategies put forth in this article do not necessarily reflect the views of Capitalism.com or Ryan Daniel Moran and should in no way be viewed as an endorsement for Mark Edward Lewis or his services.