A Quick Guide to Cognitive Bias for Investors

“If you’re so smart, why aren’t you rich?” It’s a question that rankles budding entrepreneurs, coding nerds, retirement investment enthusiasts, and paralysis-by-analysis geeks.

The goal of this piece is to make you aware of the myriad cognitive biases that plague our thinking. Hopefully, you’ll get used to asking yourself one question:

“Am I thinking about this correctly?”

Easier said than done, I know.

What's behavioral finance?

As Meir Statman puts it, “Standard finance people are modeled as ‘rational,’ whereas behavioral finance people are modeled as “normal.”

Behavioral finance became a standalone field because standard finance couldn't explain many market anomalies. There were far too many crises for standard finance models.

Check out this list of economic crises since the 1929 stock market crash. (And I’ve whittled it down to the more famous ones!)

- Wall Street Crash of 1929 and Great Depression (1929–1939)

- 1970s energy crisis

- OPEC oil price shock (1973)

- Japanese asset price bubble (1986–1992)

- Black Monday (1987) (US)

- Savings and loan crisis 1986 to 1995 in the U.S.

- Early 1990s Recession

- 1994 economic crisis in Mexico

- 1997 Asian financial crisis

- 1998 Russian financial crisis

- Argentine economic crisis (1999–2002)

- Dot-com bubble (2000-2002) (US)

- 2007-2009 Financial Crisis

- Late-2000s recession (worldwide)

- 2000s energy crisis (2003-2009) oil price bubble

- Subprime mortgage crisis (US) (2007-2010)

- Automotive industry crisis of 2008–2010 (US)

- 2008–2012 Icelandic financial crisis

- 2008–2010 Irish banking crisis

- Russian financial crisis of 2008–2009

- European sovereign debt crisis (EU) (2009-2019)

- Greek government-debt crisis (2009-2019)

- 2015 Chinese stock market crash

- Turkish currency and debt crisis, 2018

- 2020 stock market crash (2020-)

25 messes are listed here. There are many more less famous ones, as well.

But Wall Street was so enamored of its own intelligence that it took a pair of psychologists to show us the cognitive biases tricking our brains. They are Daniel Kahneman and Amos Tversky. Daniel Kahneman was awarded the Nobel Prize in Economics in 2002, even though he is a psychologist. (Tversky died in 1996. The Nobel committee doesn’t give the award posthumously.)

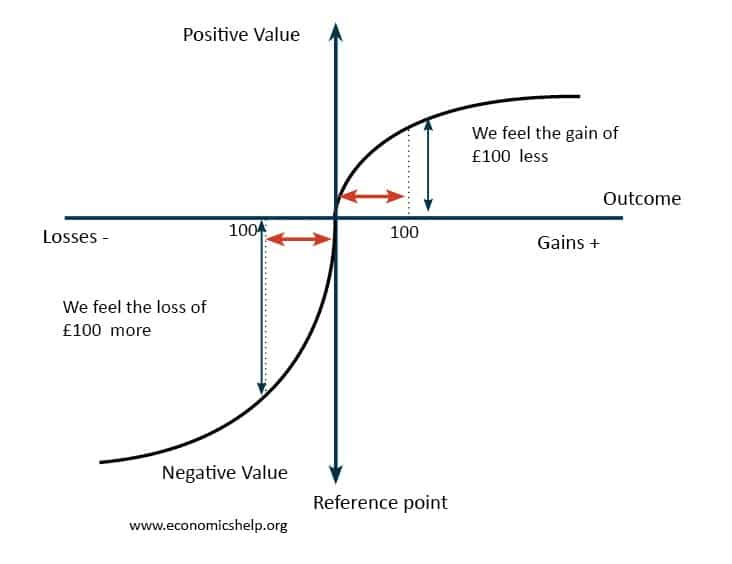

Prospect Theory

Kahneman and Tversky’s main finding is called Prospect Theory. Prospect Theory talks about how people take risks when they are losing but become more risk-averse when they're winning. Standard finance expects that to be a linear relationship. But as you can see below, it's not a linear relationship at all.

Photo Credit: EconomicsHelp.org

That reminds me of my first trade. Back in the late 90s, I sank my life savings, then $3,900, into Ciena Technologies. CIEN was trading at $39 a share, and I bought 3,900 bucks worth of shares. I had never been so nervous in my whole life. Then by some miracle, the stock price increased to $46.

I was so proud of myself. I made a $700 profit and closed my position.

Much to my chagrin, six months later, CIEN was trading at about $165 a share. I didn't get to participate in all that upside, because I got too nervous once I made a measly $7 per share.

That is what Prospect Theory is all about. I took the risk off the table when I was winning. I should have ridden that trade much higher. That’s something trend followers routinely do, but my cognitive bias got in my way.

We feel roughly 3x worse over losses than we feel happy over gains. We’ll talk more about that later.

Now, let’s define cognitive bias.

What is cognitive bias and how can it wreck my retirement investment plans?

Cognitive bias is a systematic pattern of deviation from rationality. Individuals create their own subjective reality from the information they perceive.

An individual's tailored construction of reality becomes their version of reality. And that‘s what dictates their behavior in the world. So these cognitive biases lead to perceptual distortion, inaccurate judgment, logical fallacies. They all fall under the term “irrationality.”

You can see on the cognitive bias codex below all ways you can make these mistakes. It looks painful! So instead of zooming in on this and trying to read this very fine print, we’ll explore the main biases in investing.

Every Single Cognitive Bias in One Infographic

Photo Credit: VisualCapitalist.com

But first, let's talk about how cognitive biases affect our decision making.

How do cognitive biases affect decision making?

Tversky and Kahneman introduced cognitive biases in 1972. It grew out of people's experience not with illiteracy, but with innumeracy.

Innumeracy is the lack of ability to reason and apply simple numerical concepts. We seem not to be able to reason intuitively when it comes to higher orders of magnitude.

Kahneman and Tversky demonstrated several ways that human decisions differ from rational choice. Rational choice theory had dominated standard economics for close to a century.

Kahneman and Tversky showed differences in judgment and decision-making because of heuristics. “Heuristics” is a fancy word for mental shortcuts or rules of thumb. They provide us with quick estimates about the possibility of uncertainty.

They're invaluable from an evolutionary perspective. Because when a saber-toothed tiger is chasing you, you don't have time to think about it. You've just got to run.

But they do lead to severe and systematic errors when it comes to more complicated problems. That is, when we move past rudimentary thinking and we get into more complex questions, we should stop using heuristics and think more deeply.

Kahneman and Tversky's theories are the accepted standard-bearers in behavioral finance. Others disagree. Gerd Gigerenzer, a German psychologist, argues that heuristics should not lead us to think that cognitive biases hurt us. But that we conceive rationality as an adaptive tool that is not identical to the rules of formal logic or probability.

And with all the neuroses of investors, the market isn’t always logical.

Now let’s explore those biases.

What are the most common cognitive biases?

In this section, we’ll give you some cognitive bias examples that primarily pertain to finance and investing.

Before you read this, a word of warning, you’re human. You may shudder, thinking, “I’ve made that mistake. And that one! Oh, and that one, too! I’ll never reach my retirement investment goals!” Don’t beat yourself up. The best thing you can do is learn about these biases and pause before you make any big decisions. Your awareness of bias helps to minimize them, if not outright eliminate them.

So without further ado, here they are:

Anchoring Bias

I have a friend named Harry. Back in the late 90s, he invested in what was then called Priceline.com. He bought that stock at $77 per share. During the dot-com bust, that share swiftly fell to about $7.

Now, old, stubborn Harry was not about to admit his mistake and cut his losses. He hung onto those shares for another five years or so before Priceline.com hit $77 again.

Victory? Well, he was so pleased with himself that he broke even.

However, Priceline.com is now called Booking.com. And at the time of writing, it’s trading at $1,393 a share.

How does anchoring apply to Harry?

The anchoring heuristic refers to the tendency to rely on the first piece of information received before making a decision. That first piece of information - usually the buy price - is the anchor.

It’s much better to cut your losses when you know you’re wrong than to wait for a stock that may never actually come back to the buy price.

Harry got lucky. The stock did recover… but not for years!

And then he was wrong again… by not hanging onto it longer.

It would’ve been far better to cut his losses early and then to revisit the stock when it was recovering.

Yes, that’s easier said than done.

Attentional Bias

Attentional bias is selective attention that restricts the flow of information.

Again, this is a handy human concept. If we could take in and process all the information that we see, we would all be in mental institutions.

But when it comes to investing, this isn’t a feature; it’s a bug. When we restrict the flow of information, we aren’t trading on all available information. And that leads to terrible retirement investment decisions.

Availability Heuristic

The availability bias is when easy examples come to mind, and we stop there. Or we may have forgotten about the time that something terrible happened. So, we are just using things that are readily available to us right now without taking in the full field of information.

A simple example is when investors choose their mutual funds based on the amount of advertising they do. Great funds often do no advertising at all. But the research into those funds is quite hard, so the investor will just go with the one he sees on the billboard.

Bandwagon Effect

Photo Credit: UKShop.economist.com

Kal's cartoon above is one of the most famous in financial history. The bandwagon effect is otherwise known as groupthink. Groupthink is when investors herd together. That tends to lead to huge upswings and downswings in prices, and we usually get out of our position at the wrong time.

A variant of the herd effect is cascading. Cascading is when you follow the herd even though you haven’t done your research. If someone you like listens to a financial pundit for stock picks, you may follow that advice for no other reason. Then a friend may also follow what you’re doing even though they haven’t done their research. If that pundit is wrong, you all lose.

Belief Perseverance

Belief perseverance is sticking to your original belief no matter how much evidence contradicts it. It’s rooted in cognitive dissonance. That's when you experience mental discomfort because new information clashes with existing beliefs.

There are a few different types of belief biases. Let’s explore 3 of them.

Confirmation bias

This is probably the most widespread bias of them all. Confirmation bias is when you have an idea about where a stock is going, you will only listen to evidence that confirms your belief and ignore any contradicting evidence.

A consequence is that it causes folks to hold investments too long because they're overconfident. And as a result, they're not diversified enough. Think about how Enron shareholders were getting second mortgages on their houses to buy more Enron stock… right before it collapsed!

Hindsight bias

“I knew it. I saw it all along.” And most of the time, in hindsight bias, you didn't see anything. Hindsight genuinely is 20/20. The main problem with hindsight bias is that it leads people to conclude that they can accurately predict events. You see this with analysts quite often. And hindsight bias also leads investors to be hypercritical of others.

Representativeness heuristic

Representativeness bias is when we judge the probability of an event under uncertainty.

For example:

Michael is an opera fan who likes walking around art museums. While he was growing up, he played chess with his family members and friends.

Which is more likely?

- Michael plays trumpet for a major symphony orchestra.

- Michael is a farmer.

If you chose number 1... congratulations, you’re human!

As of October 2018, there are only 108 trumpet players in the world’s major symphony orchestra. The odds are enormously against him playing the trumpet for a symphony orchestra.

Being a farmer is far more common. As of October 2019, there are over 3 million farmers in the United States alone. Number 2 has a much higher probability of being correct.

So next time you’re about to make fun of someone living in the so-called “flyover states,” you may want to buck up on your chess game!

Another variant of this is the Linda Problem or the conjunction fallacy.

The Linda Problem

We have Kahneman and Tversky to thank for this gem, as well.

Linda is thirty-one years old, single, outspoken, and very bright. She majored in philosophy. As a student, she was deeply concerned with issues of discrimination and social justice, and also participated in antinuclear demonstrations.

Which alternative is more probable?

- Linda is a bank teller.

- Linda is a bank teller and is active in the feminist movement.

Kahneman wrote in Thinking Fast and Slow, “About 85% to 90% of undergraduates at several major universities chose the second option, contrary to logic.”

Quickly, let’s say Linda has a 50% chance of being a bank teller. For those two options to be equal, Linda would have to have a 100% chance of being active in the feminist movement. (50% * 100% = 50%) Other than death and taxes, nothing’s 100%.

Fellow one-percenters, if you want to read a fun article about how AOC and her crew get this wrong, head to The Linda Problem and Why Democratic Socialists Flunk Logic 101.

Disposition Effect

The disposition effect is what I was talking about before with my first trade.

You buy a stock, you're winning on the trade, and then you cut that winner too soon. Happens all the time. You're afraid of holding it too long and losing on that trade. You love feeling right.

But the other more insidious effect is when you're holding on a trade, and you refuse to cut that trade, even though you know you’re wrong. Bitcoin traders who bought at $15,000 and above know this feeling well. They are still praying...

That’s why most traders nowadays have gone to a systematic process. They enter into a stock position and will bracket that position with an OCO order (One Cancels Other). So you may buy, say, IBM stock at a certain price.

And then once you've bought the stock, you will have a take profit level above it and a stop level below it.

And when either one of those orders is activated, that order cancels the other order, so you close the position properly.

You will either take profit if the stock goes up, which will make us very happy. Or cut our losses without us having to touch your phones or keyboards... if you were incorrect.

Ace Greenberg, who used to run Bear Stearns, credits that with his rapid promotion and rise throughout the bank. He was able to take small losses on his losing trades while riding massive winners.

Here’s a quick example:

Buy 100 IBM shares paying 123.00 per share.

Once that trade is executed, you enter an OCO order:

Sell 100 IBM shares @ 147.50 OCO Sell 100 IBM shares @ 113.16 STOP

That second order will either fill you @ 147.50 (roughly a 20% profit) and cancel the stop automatically.

Or, it’ll fill you at 113.16 for an 8% loss and cancel the sell @ 147.50 automatically.

This is a great way to manage your risk - and you don’t have to watch your screen 24/7.

Here is Interactive Broker’s way of executing OCOs.

Framing Bias

Framing bias is widespread in finance, and this is why CEOs control their EPS numbers as best they can. CEOs will lower earnings expectations between quarterly reports to manage their stock price.

An example of framing:

In Q2, our earnings per share were $0.50 compared to expectations of $0.53. Now, that would probably lead to the stock getting crushed, because they missed their earnings target by two ticks.

But let's say, in Q2, our earnings per share was $0.50, same number, compared to Q1 where they were $0.48.

So it looks like they've increased earnings over time.

This is why CEOs need to try to maintain a handle on earnings expectations. Stocks can get sold irrationally by investors who want to play beat-the-number every quarter. Jack Welch was an expert at this.

Primacy Effect

The primacy effect is also an interesting problem for a lot of investors. Primacy means that you tend to remember the earlier days. You remember older information better than more recent information. For example, a 250-point move in the Dow Jones Industrial Average is not such a big problem anymore. Back in 1987, 250-point moves were a big problem. So, you don't want the primacy effect to bias your expectations about the markets right now. The opposite of the primacy effect is recency bias.

Recency Bias

Daniel Craig is not a better Bond than Sean Connery. LeBron James is not better than Michael Jordan. All right, maybe Tom Brady is better than Joe Montana. But thanks to my age, I'll never admit to that.

Recency bias is when we place more weight on recent information and forget about history. So what you want is a delicate balance between primacy and recency to objectify your analysis.

Survivorship Bias

Elon Musk. Ray Dalio. Steve Jobs. Bill Gates. Mark Zuckerberg. They make it look so easy.

But the fact of the matter is this: in highly competitive careers, only the winners get profiled.

There is much less focus on people who may be just as skilled and determined but fail. The overwhelming majority of failures are not visible to the public eye. We only see those who've survived the pressures of their careers.

This is especially true of hedge fund managers in an industry where more hedge funds closed in 2019 than opened. The question you should ask yourself is, “How many failures am I not seeing?”

Tying It Up

You now know about Kahneman and Tversky, Prospect Theory, and some of the myriad cognitive biases that plague our thinking.

The goal of this article is not to make you look in the mirror and feel inferior or wonder about the fragility of human existence. It’s not to leave you questioning every decision you’ve ever made, or whether you’ll ever reach the point of financial independence so you can retire early.

It’s to arm you with the means to pause before you make big retirement investment decisions.

To ask yourself one simple question: “Am I thinking about this correctly?”

There’s power in the pause, not just for orators, but for thinkers.

Take your new weapons and wield them well. If your brain’s funny little shortcuts have steered you wrong before, know that you’re not alone. Smart investors know their vulnerabilities and do their best to work around them to make smart decisions. There’s always more to learn.

If you’re here because you want to learn more about how to build a business and invest the profits the smart way, you’ll probably devour this free mini-course we made for our community, too.