“The old saying goes: There are two constants in life, death, and taxes. I’m of the opinion that you want to do all you can to put both off as long as possible or at least minimize the pain they cause".

So says Robert Kiyosaki, author of the popular book Rich Dad, Poor Dad.

You see, everyone out there is looking out for tax loopholes. You’re working your tail off building a business, but if you’re not careful, your tax bill will eat your profits and leave you nothing but crumbs… so it makes sense to look for ways to minimize it a bit. And you’re in good company.

A study by Institute on Taxation and Economic policy, on corporate securities filings found 55 of America's largest companies paid no income taxes in 2020 despite generating hefty profits while netting $3.5 billion in aggregate tax rebates. Nearly half of those companies paid no U.S. income taxes for three successive years. They use accelerated depreciation, the offshoring of profits, generous deductions for appreciated employee stock options, and tax credits to scale through.

Apple made a whopping $74 billion from 2009-2012 on worldwide sales (excluding the Americas) and paid almost nothing in taxes to any country.

Big business owners like Elon Musk and Jeff Bezos are paying a very little amount of tax. The question is – can you do the same? What are tax loopholes? How not to pay taxes? What are loophole examples? And how are these big companies and business owners tax free?

In this article, you'll discover tax loopholes the rich use to pay zero taxes.

What Are Tax Loopholes?

Tax loopholes are tax law provisions that allow you to reduce the amount of tax you pay.

“Taxes are your largest single expense” says Robert Kiyosaki. So what's one of the best ways to decrease your largest single expense? The answer is tax loopholes - but what is a tax loophole?

According to dictionary.com, A tax loophole is a provision in the laws governing taxation that allows people to reduce their taxes.

The term has the connotation of an unintentional omission or obscurity in the law that allows the reduction of tax liability to a point below that intended by the framers of the law. Still, when interpreted and used correctly, they are 100% legal.

How Do The Rich Use Tax Loopholes To Pay Taxes?

The top 1% of Americans may be dodging as much as $163 billion in annual taxes, according to the U.S. Department of the Treasury.

How are they doing it?

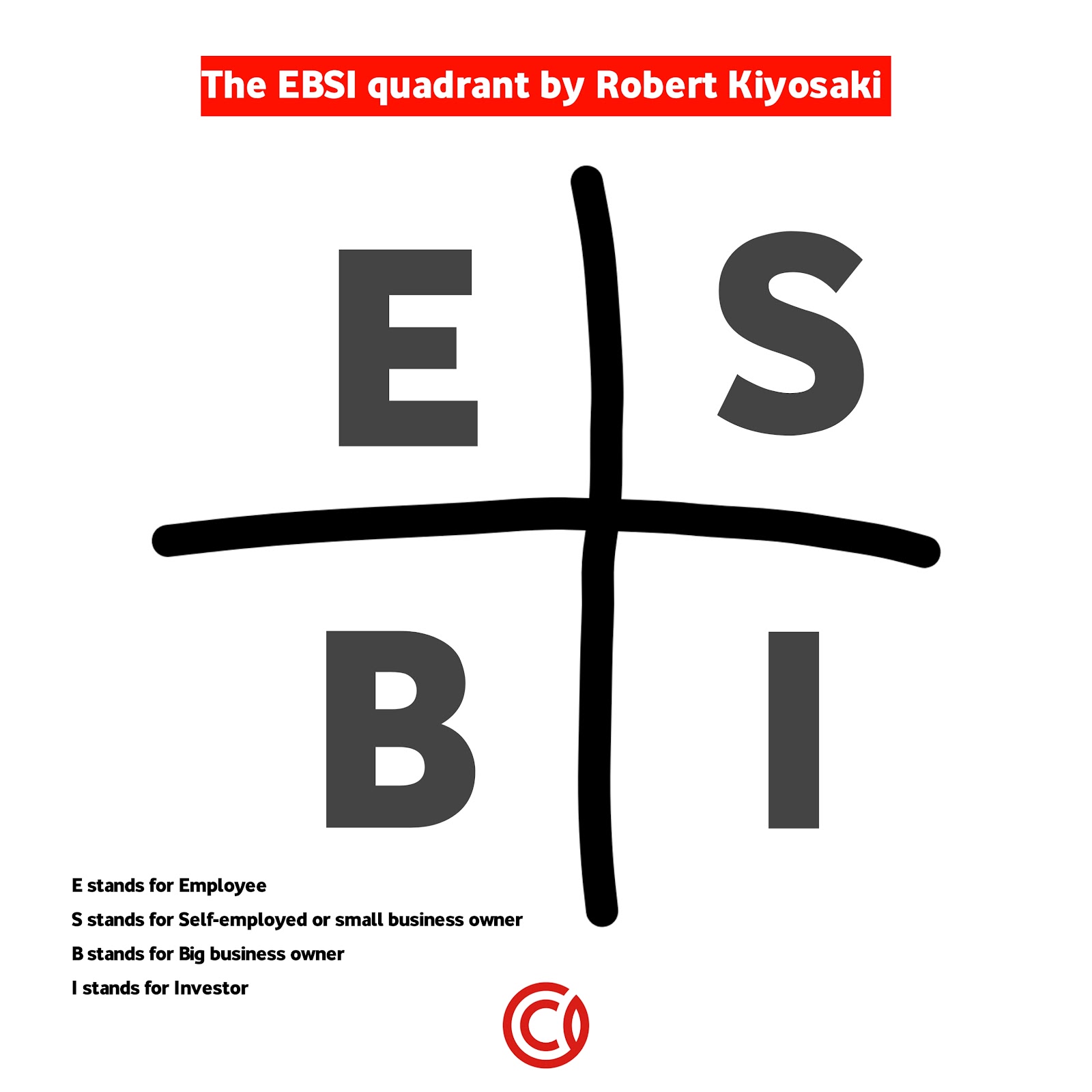

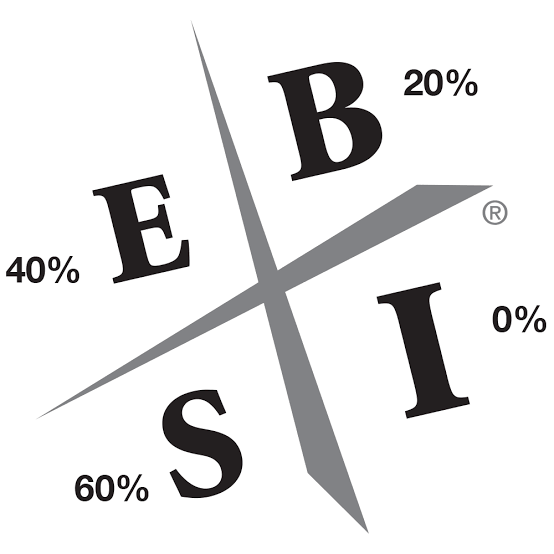

Take a look at Robert Kiyosaki’s Cash Quadrant, and you’ll see something fascinating.

Remember this? We’ve got Employees, Self-Employed (or Small Business Owner), Big Business Owner, and Investor.

As you can see, the tax rates of the Investor and the Big Business Owner are low compared to that of Employees and small business owners. But why is this so?

The Big Business Owners and Investors have found loopholes to take advantage of – loopholes anyone in business should consider and discuss with their tax strategist.

We’ll get into those loopholes in a moment, but first, you may be wondering why we’d encourage business owners to look for ways to reduce - or even eliminate - their business tax bill.

Here’s why:

As Ryan Daniel Moran says “Listen, I don't care how much money you make. I don't care what good you think the government does. Money in people's pockets is always better spent than handing it off to politicians who don't know who you are, probably don't care who you are, and are out of touch with the solutions that make a change in the world.”

You might also want to read this argument against increasing the tax rate for high income earners.

Tax loopholes in a nutshell: If you take the money that you make in your business and you reinvest it to produce more goods and services to build your business, guess what? You can minimize or even entirely delete your tax bill.

But unfortunately, here's what most people do in business: When the business makes money, they spend it. What happens next? They're taxed heavily. (Want to see what happened when Ryan wrote a check for $170,000 for his tax bill?)

If you sell physical products, you’re going to want to watch this video from Tom Wheelwright of Wealthability.

He shares the four rules you must abide by to play a smarter game of tax strategy:

- You have to be under $25m of gross receipts

- You must elect to be on the cash method of accounting

- You have to elect to treat your inventory as non–accidental materials

- You have to do a de minimis election.

If you meet those conditions in your business, it’s time for a conversation with your accounting team to see how you can use the strategies Tom lays out in that video.

Tax Loopholes: What Are They? And How Do They Work?

There are many tax loopholes used by the rich and high-income earners to pay little to no taxes. You may be able to use them, too. Just check with your tax strategist first.

#1: Save on your taxes by covering medical bills past, present, and future.

Have you ever heard of the Health Savings Account (HSA)? With HSA, you can effectively deduct your medical expenses from the first dollar as far as you have a highly deductible insurance plan.

Now, you no longer have to worry about paying taxes for your present and future medical expenses. Funds in your HSA can be used to pay for any medical expenses that occur after you open the account, regardless of when contributions were made according to gobankingrates.

#2: Save when you sell real estate.

In real estate, one expert level tactic is the 1031 Exchange, also known as the secret Donald Trump and other real-estate developers use to pay almost nothing in taxes.

The stepped-up basis loophole allows someone to pass down assets without triggering a tax event, which can save estates considerable money. It does, however, come with an element of risk. If the value of this asset declines, the estate might lose more money to the market than the IRS would take.

How’s it work? When you inherit a house, the current IRS tax code gives you a stepped-up basis in cost. Your stepped-up basis is the market value on the date of your benefactor’s death.

Here's an example showing the stepped-up basis: Joe bought a house 25 years ago for $150,000. Now, the house is worth $1 million. If Joe were to give the house to his first son (while Joe is still alive), the son's cost basis in the house is $150,000. If the son sells the house for $1 million, he would pay capital gains on $850,000.

However, if his father decides to hold on to the house and give the property to his son in a will, then the magic of the stepped-up basis kicks in. The stepped-up basis magically allows his son to “step up” his cost basis to $1 million, he would pay ZERO capital gains taxes to the IRS if he sold it. The stepped-up basis works for both principal residence and rental property.

#3: Breast augmentation = tax reduction? Let's find out!

Are breast implants tax deductible? Recently the IRS considered breast implants as cosmetic surgery, so they do not qualify as medical expenses. But what about professional stippers? You could argue that breast implants are a work expense in that case… maybe. Definitely worth asking your tax professional.

#4: Work from home in your pajamas and save on your taxes.

If you use a section of your home solely for business purposes, then you are qualified for the home office deduction. A home can include a house, a mobile home, or even a standalone structure.

For the tax year 2022, the rate for the simplified square footage calculation is $5 per square foot, with a maximum of 300 square feet.

But then there are factors to consider. Is your home the principal location of your business? And do you use it often to interact with and meet customers?

You will need to figure out the percentage of your home that is dedicated to your business. For example, if your home is 1,000 square feet and your office is 200 square feet, then you can deduct 20% of your mortgage, insurance, and utilities from your taxes.

The home office deduction can be a great way to lower your taxable income and save money on your taxes. Be sure to talk to your tax advisor to see if you qualify.

#5: Be your own boss and fire your tax bill.

A “1099 employee, ”, or independent contractor is a person who offers services to different clients. ”

Their services are independent of the company so they only get paid for the work they perform but do not have some benefits and deductions that W-2 employees (salaried workers) would receive from an employer…

So what's the 1099 tax loophole about?

The tax bill that comes with 1099 income is huge. When you work as a W-2 employee for a company, you automatically have 7.65% of your income withheld from your paycheck for taxes.

This is known as FICA and covers: Social security and medicare taxes. It’s a huge help when tax time comes around because it means you’ve already paid a good chunk of your taxes throughout the year.

The first step to reducing your tax is to write off all eligible expenses. Use your self-employment health insurance to save on income taxes. Put money in your retirement accounts. If you qualify, get paid through an S corp. How do you qualify to get paid through an S corp?

Firstly, you must attain a certain status of eligibility, you must notify the IRS of their choice to be taxed within an explicit time period and you must have no more than 100 shareholders to qualify as an S-corporation.

#6: Holding a meeting for your business? Rent meeting space in your house, and save on your taxes.

The Augusta Rule Section 280A(g) states in part:

“…if a dwelling unit is used during the taxable year by the taxpayer as a residence and such dwelling unit is rented for less than 15 days during the taxable year, then… the income derived from such use for the taxable year shall not be included in gross income…

In simple terms, this means that renting a room in your home is not taxed.

#7: Look to life insurance for a loophole your heirs will appreciate.

Life insurance allows you to transfer a policy's death benefit income-tax-free to beneficiaries. No matter how big the death benefit is—$70,000 or $50 million—your beneficiaries won't pay a single cent of income tax on the money they get. As simple as that.

#8: Put on a song and dance, take a tax break.

If you are a qualified performing artist, you can deduct performing–arts–related business expenses even if itemization of deductions is not allowed. You must have worked for two employees at a rate of $200 or more in a year to qualify.

#9: Want to live on a yacht and save on your taxes?

You can classify your boat as a first or second home and save on your tax bill while living the dream. Or, you can just use your boat for business meetings as long as you keep good documentation. There are just three qualifications you need to meet:a sleeping berth, cooking facilities, and a toilet facility aboard. Tired of being a boat owner? You can donate it and get tax benefits.

#10: Sin impuestos! (‘No taxes’ in Spanish).

“A lot of people are moving to Puerto Rico," says social worker Melissa DaSilva in my newest video. Two years ago, she ran a therapy business in Rhode Island. Now she runs it remotely from Puerto Rico. "I'm saving 25 percent of my income." Now, a lot of people are moving to Puerto Rico to build businesses because of the tax break initiated by a politician.

#11: Save on your taxes when you give this gift.

You can maximize a critical loophole in I Bond gifts. Although each individual can only purchase $10,000 in I bonds each calendar year there’s a loophole: Those who use their ,federal income tax refunds can buy an additional $5,000, bringing the total to $15,000.

#12: Save on the pass-through income from your business if you’ve got the right entity in place.

QBI deduction "allows non-corporate taxpayers to deduct up to 20 percent of their QBI, plus 20% of qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership (PTP) income." We explained all you need to know about QBI in this article.

The Tax Cuts and Jobs Act created a deduction for households with income from sole proprietorships, partnerships, and S corporations, which allows taxpayers to exclude up to 20 percent of their pass-through business income from federal income tax

FAQs

What are tax loopholes?

Tax Loopholes are simply provisions made in the tax code for citizens both poor and rich to reduce their income taxes legitimately.

Tax Loopholes: Who uses them?

Many people think tax loopholes are just for the rich alone. No! Tax loopholes are also for the poor and every other citizen. From singles to married couples, corporations, etc.

Are tax loopholes legal?

Tax loopholes are legal if used appropriately. As earlier stated in the definition of a tax loophole, it is a provision in the tax code that allows you to reduce the taxes you pay.

Tax Loopholes: Are there any risks?

There are no risks associated with tax loopholes as long as you use them correctly. The goal is to avoid but not evade taxes. Your tax strategist can help ensure you don’t pay a penny more than you owe.

What tax credits can you use if you own a business?

There are many tax credits model to maximize for your business, here's a list of tax credits:

What are the different types of tax loopholes?

There are other types of tax loopholes worth checking out:

What are the benefits of using a tax loophole?

One of the most important benefits of a Tax loophole is that it increases your savings and investment resources.

What is the difference between a tax deduction and a tax credit?

First, let's define what a tax deduction is. A tax deduction is a provision that reduces taxable income. A standard deduction is a single deduction at a fixed amount

A tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly.

For example, if your federal tax bill is $15,000 and you are entitled to a $5,500 tax credit, that credit cuts your tax bill by $5,500 — to $9,500.

Tax credits are incentives governments give for behaviors they want to encourage, such as installing solar panels, purchasing an electric vehicle, or adopting a child.

So what are the differences? The table below explains it all

| Tax Deduction | Tax credit |

| It is available before the imposition of credit | It is applicable after deductions are taken |

| Tax deductions are available either as itemized deductions or the standard deduction | Tax credits are either non-refundable or refundable |

How do I know if I am eligible for a business tax loophole?

Are you 18+? Do you own a corporation or business? If you tick yes for these questions then you may be eligible. Check with your tax professional.

What are the income restrictions for tax loopholes?

The income restrictions for tax loopholes vary based on the diverse examples in this article and other online resources. Even so, according to Tom Wheelwright, you have to be under $25m gross receipts to benefit.

What is the difference between a tax loophole and a tax shelter?

A tax shelter is any legal strategy you employ to reduce the amount of income taxes you owe.

While a tax loophole is a tax law provision or a shortcoming of legislation that allows individuals and companies to lower tax liability.

The Takeaway

As Tom Wheelwright says, the entire tax code serves as a rulebook the government has created to show you how to decrease (or even delete) your tax bill. The goal is never to evade taxes, but to avoid paying any you don’t need to pay.

To take maximum advantage of legal tax loopholes, you and your tax strategist must be aware of the rules and follow them. Your current tax preparer might be willing and able to help you slash your tax bill using this strategy. But if not, it may be time for an upgrade to get more strategic professional services. Many in The One Percent community rely on Tom Wheelwright’s team to ensure they don’t pay a penny more in taxes than they must.